Over the past six months, Robert Half’s shares (currently trading at $55.99) have posted a disappointing 15.8% loss while the S&P 500 was down 3.3%. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Robert Half, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free .

Even though the stock has become cheaper, we don't have much confidence in Robert Half. Here are three reasons why there are better opportunities than RHI and a stock we'd rather own.

Why Do We Think Robert Half Will Underperform?

With roots dating back to 1948 as the first specialized recruiting firm for accounting and finance professionals, Robert Half (NYSE:RHI) provides specialized talent solutions and business consulting services, connecting skilled professionals with companies across various fields.

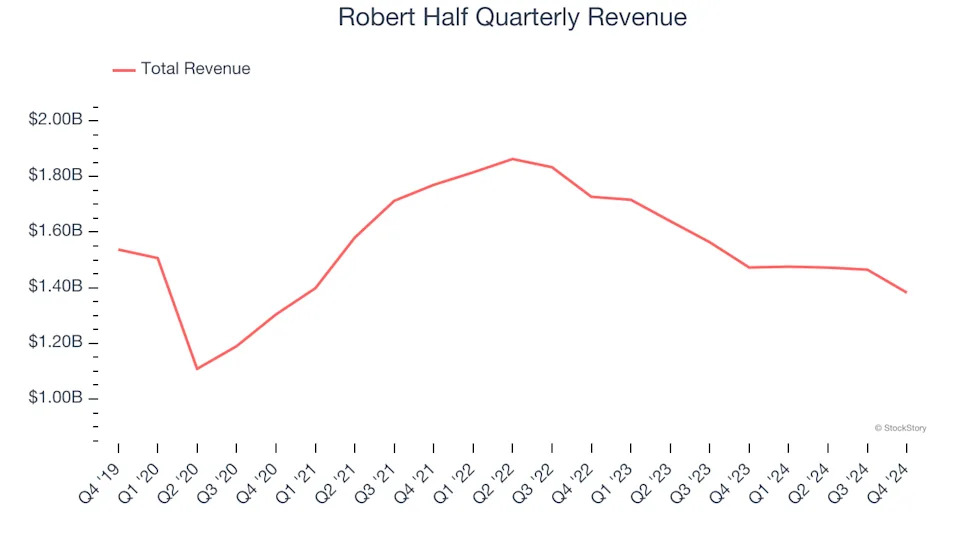

1. Long-Term Revenue Growth Flatter Than a Pancake

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Robert Half struggled to consistently increase demand as its $5.80 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a low quality business.

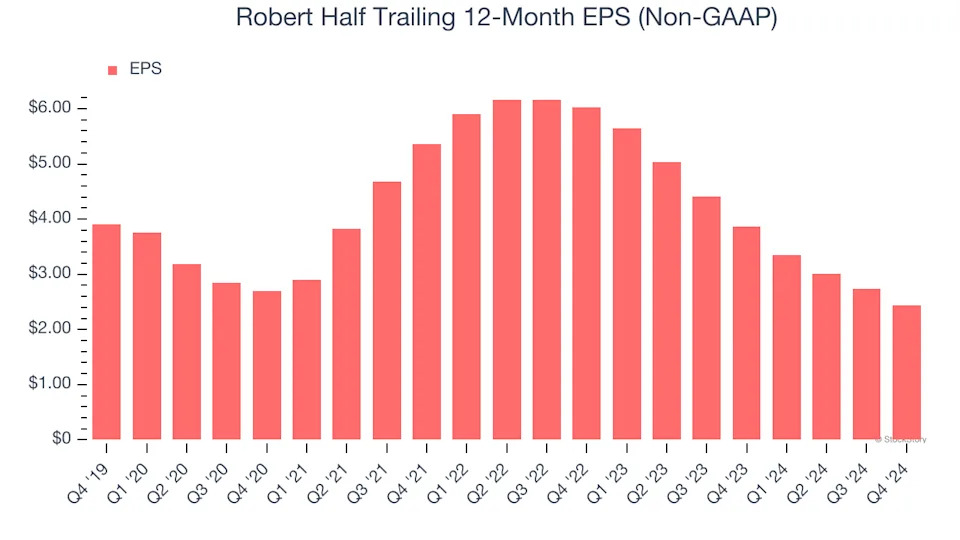

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Robert Half, its EPS declined by 9% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

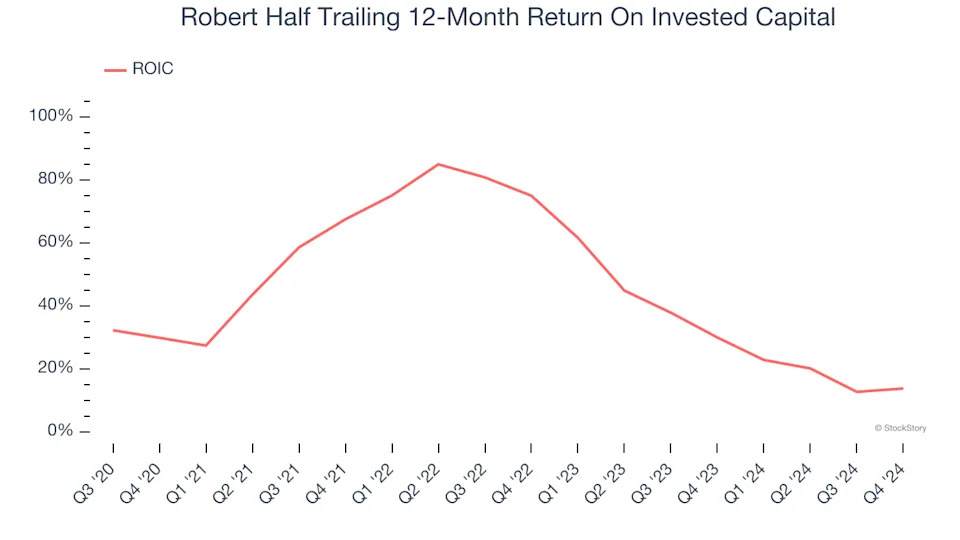

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Robert Half’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

We see the value of companies helping consumers, but in the case of Robert Half, we’re out. Following the recent decline, the stock trades at 18.2× forward price-to-earnings (or $55.99 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at our favorite semiconductor picks and shovels play .

Stocks We Like More Than Robert Half

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Strong Momentum Stocks for this week . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .