(Bloomberg) — A month ago, all anyone in markets could talk about was Donald Trump and how his blueprint for the US economy would sow growth, next year and beyond.

Heading into the Christmas break, a no-less-formidable force has retaken the stage: Jerome Powell. The Federal Reserve chair’s hawkish turn this week put inflation back on the map as investors’ obsession of choice, spurring the biggest moves — up and down — since just after Election Day.

First it was Wednesday, when Powell voiced waning enthusiasm for interest-rate cuts and sent stocks and bonds to their worst sessions in months. Then moods improved significantly two days later, when the Fed’s preferred inflation gauge showed prices rising less than forecast, spurring a cross-market rally that helped trim the S&P 500’s weekly loss.

Feeding the extreme moves is high-conviction positioning, much of it by investors wagering the Trump trade has further to run in risky assets. Allocations to US equities jumped to a record while cash holdings all but evaporated, according to Bank of America Corp.’s global fund manager survey. Even systematic players such as volatility-controlled funds were piling into stocks.

The gyrations are a reminder that while it was Trump who sent speculative spirits soaring, the trajectory of inflation — and Powell’s reaction to it — loom just as large in markets where hand-over-fist buying has sent measures of valuation to extreme levels. Even with Friday’s rebound, the benchmark US equity gauge slid about 2% over the five days, while post-election stalwarts like small caps and value stocks slid a third week.

“Investors found themselves thinking that the Fed would lower rates, no matter what,” said Sameer Samana, senior global market strategist at Wells Fargo Investment Institute. “The disappointment was that the Fed finally woke up to the fact that inflation had stopped coming down.”

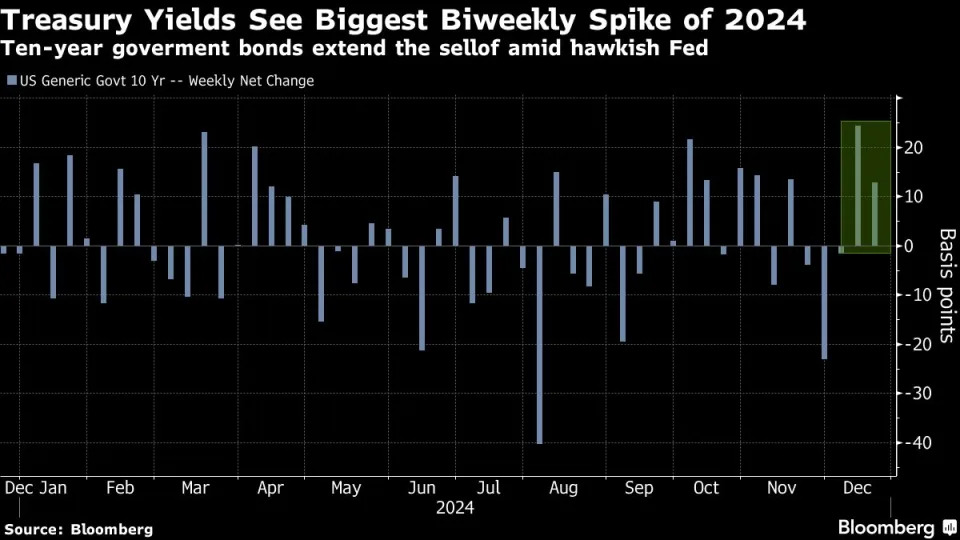

For now the last remnant of the Trump trade is the leg that many investors wanted least: rising bond yields. Rates on 10-year US Treasuries jumped to the highest in seven months. Driving the move were diminishing bets on interest-rate cuts after Wednesday’s Fed meeting, at which officials predicted fewer would be appropriate given inflation’s nagging presence.

That set the stage for pain on Wednesday, when moderately hawkish comments by Powell translated into a full-blown selloff, including the worst fall for the S&P 500 on any regularly scheduled Fed decision day since 2001. Per the Fed chief, policymakers must see further progress on inflation before easing further.

Signs of fatigue were evident even at the market’s hyperactive edges. Bitcoin, whose straight-up route has been a hallmark of Trump euphoria, fell back below $100,000, sending Michael Saylor’s MicroStrategy Inc. down more than 10%. A closed-end fund that owns private-company stakes, Destiny Tech100 Inc., slid about 15%, while the ARK Innovation ETF saw its biggest outflow in a month in the wake of the Fed meeting.

“There were a lot of people, even people who expected a hawkish Fed meeting, who were surprised,” said Max Gokhman, senior vice president at Franklin Templeton Investment Solutions. “Then, the tug and pull kind of came back between those who believe that we’re going to unleash the animal spirits through the new president’s agenda and those who think that there is going to be significant inflation that’s unleashed instead, and that actually is going to drive down stock prices.”

In short, investors who grew euphoric over Trump’s tax-cut and deregulation promises now must balance the outlook with a more tangible risk that inflation has yet to be subdued, courtesy of Powell. The Fed chief stopped short of implicating the president-elect’s policy priorities in the central bank’s toughening inflation posture — but didn’t completely dismiss them, either.

Fear Gauge

Confusion over which input to heed has been a recipe for cross-asset volatility. The VIX, Wall Street’s “fear gauge,” spiked above 28 on Wednesday, a level not seen since August, only to settle back below 20 on Friday. Ten-year Treasury yields went nine straight days without falling through Thursday, then eased when the so-called core personal consumption expenditures index posted its slowest monthly advance since May.

US 10-year yields have now climbed some 37 basis point in two weeks, the biggest jump over such a stretch this year, while exchange-traded funds tracking investment-grade and high-yield bonds have slipped. In crypto, Bitcoin posted two of its worst losing sessions of the quarter on Thursday and Friday, though remains up more than 100% since this time last year.

Not everyone is getting hammered by the recent market twists. Alessio de Longis, head of investments at Invesco Solutions, said that since July, he’s held positions that profit if stocks trail bonds or defensive equities rise. Those had been painful ones to hold as investors went giddy for Trump.

“We are beginning to see that unwind already,” de Longis said. “The election trades are finding fatigue.”